Mortgage Calculator Frankfurt 🇩🇪 –

Buying Property in Frankfurt Explained

🏡 Buy Property in Frankfurt Webinar

📅 Tue 24th March — 7pm

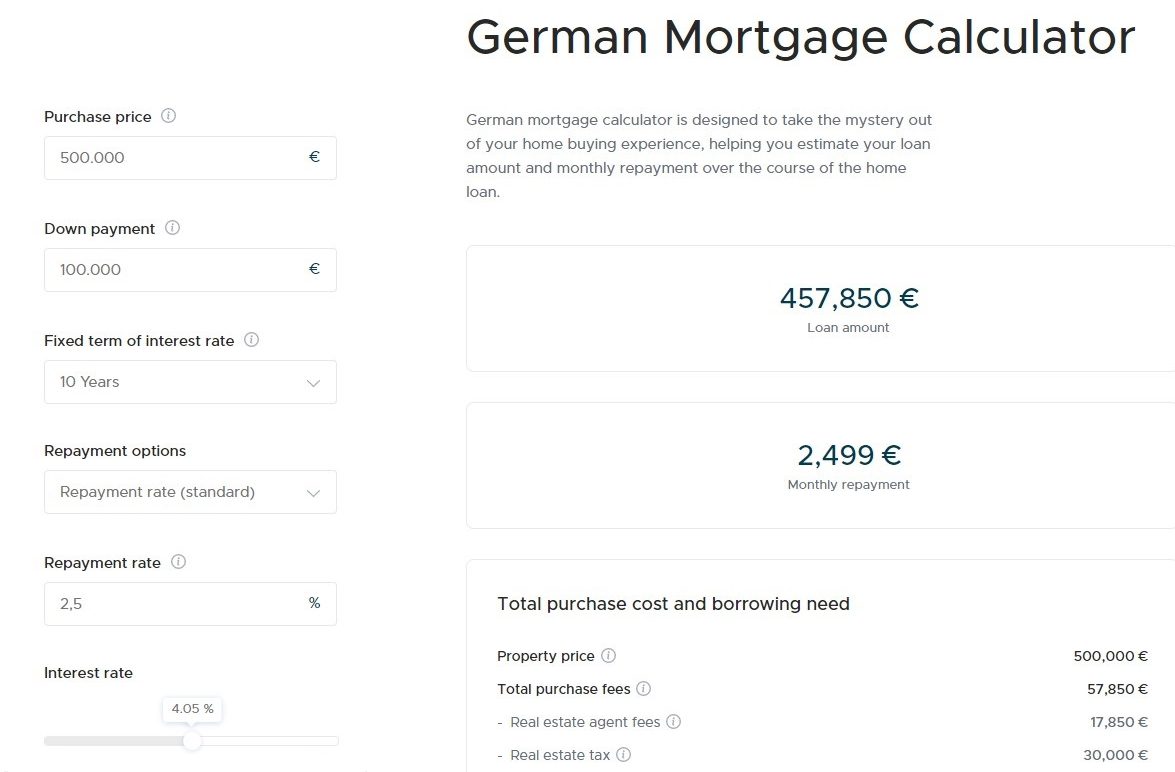

Property Cost Calculator

Estimate total purchase costs before getting your mortgage.

Can You Afford a Property in Frankfurt?

Calculate your real monthly mortgage payment, deposit and buying costs in Germany — including tax, notary and estate agent fees.

Buying in Frankfurt is not just about the purchase price

Between deposit, tax, notary fees and possible agent commission, the real cost is much higher than most first-time buyers expect. This calculator gives a much more realistic starting point.

See My NumbersEstimate your mortgage costs in Frankfurt

Adjust the sliders and options below to see your likely monthly payment and total buying costs.

Your estimated costs

What to know before applying for a mortgage in Frankfurt

1. The purchase price is only part of the story

In Frankfurt, buyers often focus on the listed property price and forget the extra costs. In Germany, these usually include property transfer tax, notary and land registry fees, and sometimes estate agent commission. That means the cash you need upfront is usually much higher than expected.

2. Your deposit changes everything

A bigger deposit can reduce your loan amount, improve your monthly payment and sometimes help you get better mortgage terms. Buyers with stronger equity are usually in a better position with lenders.

3. Expats can get mortgages in Germany

Plenty of expats buy property in Germany, but lenders usually want to see stable income, good documentation and a sensible level of own capital. The stronger and cleaner your financial profile looks, the easier the conversation tends to be.

4. Frankfurt is expensive, so planning matters

Frankfurt property prices mean small mistakes can get expensive fast. Running the numbers properly before you fall in love with a property can save time, stress and rejected financing attempts.

Explore more property resources

Mortgage questions people ask most

Most buyers should plan for around 10% to 20% deposit, plus additional buying costs. The exact number depends on the bank, your income profile and how strong your overall application is.

In Hessen, you usually need to budget for 6% property transfer tax, roughly 1.5% to 2% for notary and land registry, and possibly estate agent fees depending on the deal.

Yes. Expats can often get a mortgage in Germany if they have stable income, the right documentation, enough deposit and a financial profile that works for the lender.

It is a strong planning estimate, but not a binding mortgage offer. Real offers depend on the lender, your income, residency, expenses, deposit and the property itself.

There is no single number. It depends on the size of the mortgage, your deposit, interest rate, monthly commitments and whether you are applying alone or as a couple.

Recommended SEO blog to support this page

Buying Property in Frankfurt as an Expat (2026 Guide)

Use this article to target long-tail traffic, explain the buying process, cover hidden costs and funnel readers back into the calculator and webinar.

Read the GuideCan You Afford a Property in Frankfurt?

Calculate your real monthly mortgage payment, deposit and buying costs in Germany — including tax, notary and estate agent fees.

Buying in Frankfurt is not just about the purchase price

Between deposit, tax, notary fees and possible agent commission, the real cost is much higher than most first-time buyers expect. This calculator gives a much more realistic starting point.

See My NumbersEstimate your mortgage costs in Frankfurt

Adjust the sliders and options below to see your likely monthly payment and total buying costs.

Your estimated costs

What to know before applying for a mortgage in Frankfurt

1. The purchase price is only part of the story

In Frankfurt, buyers often focus on the listed property price and forget the extra costs. In Germany, these usually include property transfer tax, notary and land registry fees, and sometimes estate agent commission. That means the cash you need upfront is usually much higher than expected.

2. Your deposit changes everything

A bigger deposit can reduce your loan amount, improve your monthly payment and sometimes help you get better mortgage terms. Buyers with stronger equity are usually in a better position with lenders.

3. Expats can get mortgages in Germany

Plenty of expats buy property in Germany, but lenders usually want to see stable income, good documentation and a sensible level of own capital. The stronger and cleaner your financial profile looks, the easier the conversation tends to be.

4. Frankfurt is expensive, so planning matters

Frankfurt property prices mean small mistakes can get expensive fast. Running the numbers properly before you fall in love with a property can save time, stress and rejected financing attempts.

Explore more property resources

Mortgage questions people ask most

Most buyers should plan for around 10% to 20% deposit, plus additional buying costs. The exact number depends on the bank, your income profile and how strong your overall application is.

In Hessen, you usually need to budget for 6% property transfer tax, roughly 1.5% to 2% for notary and land registry, and possibly estate agent fees depending on the deal.

Yes. Expats can often get a mortgage in Germany if they have stable income, the right documentation, enough deposit and a financial profile that works for the lender.

It is a strong planning estimate, but not a binding mortgage offer. Real offers depend on the lender, your income, residency, expenses, deposit and the property itself.

There is no single number. It depends on the size of the mortgage, your deposit, interest rate, monthly commitments and whether you are applying alone or as a couple.

Recommended SEO blog to support this page

Buying Property in Frankfurt as an Expat (2026 Guide)

Use this article to target long-tail traffic, explain the buying process, cover hidden costs and funnel readers back into the calculator and webinar.

Read the GuideMortgage questions people actually ask

Typically 10%–20% of the property price, plus another 10%–15% for taxes, notary and possible agent fees. Many buyers underestimate this total cash requirement.

In Hessen you usually pay 6% property transfer tax, around 1.5%–2% notary and land registry, and sometimes up to 3.57% estate agent fees.

Yes. Most expats can get a mortgage if they have stable income, sufficient deposit and clean financial records. The stronger your profile, the better your terms.

It depends on your income, expenses, deposit and interest rate. As a rough guide, banks want your monthly payment to stay manageable relative to your net income.

It gives a realistic estimate based on German buying costs, but it is not a formal offer. Final terms depend on your profile and the bank.

Frankfurt remains one of Germany’s strongest property markets, but high prices mean getting the numbers right upfront is critical. Many buyers overpay simply by not calculating properly.

Buying Property in Frankfurt 🇩🇪 – Mortgage, Costs & What Banks Don’t Tell You

Frankfurt is one of Germany’s most competitive property markets — high demand, rising prices, and strict lending rules.

- 💰 Most buyers underestimate costs by €30k–€80k

- 🏦 Banks often approve more than you should actually spend

- 📉 Taxes and fees add 10–15% on top

📊 Real Cost of Buying in Frankfurt

- €300,000 property

- + €18,000 tax (6%)

- + €6,000 notary

- + €10,700 agent

👉 Total: ~€334,700

👉 See your real cost breakdown

📉 How Much Can You Actually Borrow?

👉 Stay within 30–40% of your net income.

❓ Mortgage FAQ – Frankfurt

Mortgage in Germany for Foreigners | Getting a house loan for Expats

If you are an expat living in Germany and have been wanting to buy a house or property but have been unable to get a mortgage, don’t worry – there is help available for getting mortgage in Germany. We offer a variety of German mortgage support and assistance programs specifically designed for foreigners, so you can finally make your dream of owning property in Germany a reality. Keep reading to learn more about these programs and how to apply.

How Mortgage Works in Germany

The first step to getting a mortgage in Germany is understanding how the process works. In general, you will need to put down a deposit of at least 20% of the purchase price of the property, and then the bank will loan you the remaining amount. The interest rate on your loan will be determined by a number of factors, including your credit score, employment history, and the type of property you are buying.

The standard loan term in Germany is 10 years, but you may be able to negotiate a longer or shorter repayment period depending on your financial situation. It is also important to note that most banks will require you to take out mortgage insurance, which will protect them in case you are unable to make your loan payments.

Mortgage Insurance

Mortgage insurance is not required by law in Germany, but most banks will require you to take out a policy before they will approve your loan. This insurance protects the bank in case you are unable to make your loan payments and default on your mortgage.

There are two main types of mortgage insurance available in Germany:

This type of insurance covers you in case you lose your job or have some other financial setback that prevents you from making your loan payments.

This type of insurance covers your mortgage payments in case you die before the loan is paid off.

The cost of the mortgage insurance will vary depending on the type of policy you choose, your age, the amount of your loan, and the length of your repayment period.

Types of German Mortgages

There are different types of mortgages available in Germany:

Variable-rate mortgage

With this type of mortgage, the interest rate on your loan will fluctuate over time in line with market rates. This can make your monthly payments higher or lower, depending on market conditions.

Fixed-rate mortgage

With a fixed-rate mortgage, the interest rate on your loan is locked in for the entire repayment period, so your monthly payments will stay the same even if market rates rise.

Interest-only mortgage

With this type of mortgage, you only have to pay the interest on your loan for a certain period of time, usually 5-10 years. After that, you will need to start paying off the principal as well.

This can be a good option if you expect your income to increase over time, as it will make your monthly payments more manageable in the short term.

Annuity mortgage

With an annuity mortgage, your monthly payments stay the same for the entire repayment period, but the amount of each payment that goes towards interest and principal will change over time.

At first, most of your payment will go towards paying the interest on your loan. But as time goes on, a larger portion of your payment will go towards paying off the principal.

This can be a good option if you want the stability of fixed monthly payments but want to pay off your loan more quickly.

Full repayment mortgage

With a full repayment mortgage, the entire amount of your loan (principal and interest) is paid back over the course of the loan term. This means that your monthly payments will be higher than with other types of mortgages, but you will pay off your loan more quickly.

This can be a good option if you have a large downpayment and want to pay off your loan as quickly as possible.

Building Society loans

In Germany, you can also apply for a loan from a building society (Bausparkasse). These are specialized banks that offer loans specifically for the purpose of buying property.

Building societies typically offer lower interest rates than regular banks, but they may require you to take out additional insurance policies or make a higher downpayment.

How You Can Buy a Property with a House Loan in Germany

If you are a foreigner looking to buy a property in Germany, there are a few things you need to know about the process.

Step 1

Step 2

Step 3

How we will assist you in this process

As your personal mortgage broker, we will be with you every step of the way, from finding the best mortgage deal that suits your needs to help you with the paperwork and application process. We have a wide network of lenders and banks that we work with, so we can find the best mortgage rate for you.

We understand that buying a property can be a stressful experience, so we will make sure that the process is as smooth and hassle-free as possible.

Mortgage Calculator

Mortgage Calculator – Ready to purchase a property in Germany?

Have Carita and Paul find the best mortgage offer for you!

Answer 10 questions, get your pre-approval financing certificate!

100% free to you €0

German Mortgage Calculator for Expats

When you are looking to buy a property in Germany, it is important to calculate how much you can afford to borrow. With our mortgage calculator, you can easily see how much your monthly payments would be and how much interest you would pay over the course of the loan.

How the home loan calculator works

To calculate your monthly payments, enter the loan amount, loan term, and interest rate into the calculator. The calculator will then give you an estimate of the monthly payments and total interest payable.

The mortgage calculator is a great tool to help you budget for your new home purchase. It can also help you compare different loan options to find the best one for you.

Does a house loan calculator guarantee that you’d receive a mortgage?

A mortgage calculator is a helpful tool, but it is important to remember that it is only an estimate. The actual loan amount and the interest rate you receive will depend on many factors, including your credit history, income, and employment status.

Requirements to Apply for German Mortage

You’ll need to gather several documents, many of which will be from several years ago, to verify that you fulfill the above requirements for your mortgage application. We can help you figure out which papers you’ll require. This usually includes:

- A form of ID (e.g. passport)

- Residence permit (if applicable)

- Registration certificate

- Proof of a German pension scheme, (e.g. social security ID)

- Proof of available equity

- Documents related to the property, (e.g. land registry extract, property assessment )

Steps Involved in a German Mortgage Process

Now that you know what you’ll need and what to expect, let’s walk through the key steps of getting a mortgage in Germany.

This step involves shopping around for the best interest rates and terms that suit your needs. It’s important to compare different offers from a range of lenders, as they can differ significantly. We’ll help you compare interest rates and loan terms from different banks and lenders.

In this step, you’ll need to gather all of the required documents for your mortgage application. This can include your passport, proof of income, bank statements, and more. We can help you figure out which documents you’ll need.

This step involves filling out a mortgage application and submitting it to the lender. The application will ask for information about your finances, employment, and property. We’ll help you fill out the application and submit it to the bank or lender.

In this step, the bank will send a valuation of the property to make sure that it is worth the purchase price.

Once the valuation has been approved, the bank will transfer the loan amount to your account and you can start the process of buying the property.

Process of Buying Property in Germany

Thinking about buying a home? We help you buying a property in Germany, we asked an expert to come up with this Guide to clearly outline what you can expect at every single step of you going through the property buying experience. If you are looking for your dream house for your family or are an investor looking into the German real estate market, the steps described in this guide will help you navigate through the process.

Mortgage Calculator will help you find out the monthly mortgage payment. Also, easily input a different home price, down payment, loan term and interest rate to see how your monthly payment will change. These Estimates are broken down by principal, interest, property taxes and homeowners insurance.

Mortgage & Property Buying Process

- Check your affordability online

- Chat with our mortgage advisor

- Finding the right property you afford

- Secure and reserving the property

- Finalizing your mortgage contracts

The most important things to consider are:

- How long term do you want to fix the interest period?

- How quickly and easy do you want to pay back your mortgage?

- Equity you put to get the best rate?

- You have full access to your new property.

Only after the vendor has received the complete amount of the acquisition amount on their checking account, you’ll arrange for the official handover of your new property.

Frequently Asked Questions

Yes, foreigners can apply for a mortgage in Germany. However, there are some additional requirements that you’ll need to meet, such as having a residence permit and proof of income.

No, buying a property in Germany does not automatically qualify you for a residency visa. However, if you can show that you have a stable income and are able to support yourself, you may be eligible for a residency visa.

Yes, EU citizens can buy property in Germany. However, they may need to obtain a residence permit and proof of income in order to qualify for a mortgage.

German mortgage rates can vary depending on the type of loan and the lender. However, interest rates are typically around 3-4% for fixed-rate loans and 2-3% for variable-rate loans.

Mortgage Calculator

Mortgage Calculator – Ready to purchase a property in Germany?

Have Carita and Paul find the best mortgage offer for you!

Answer 10 questions, get your pre-approval financing certificate!

100% free to you €0

Home Loan Calculator Germany

My Mortgage Germany UG is a certified mortgage intermediary according to §34i Abs 1, S. 1 GewO supervised by the Berlin Gewerbeamt.

Friedrichstr. 123 | 10117 Berlin | Germany

©2023 All Rights Reserved. MyMortgageGermany.de